Indian companies have record cash reserves. Banks have clean balance sheets and want to lend. Yet private Capex remains subdued.

Instead of leveraging excess cash and cheap loans to invest, companies are hoarding cash, buying government bonds, or returning money to shareholders via dividends and buybacks.

So why is this?

The usual excuse is poor consumption growth – why would companies invest when there is excess capacity? Some also blame the investment community’s focus on quarterly results and near-term RoE and cash flow, which deters companies from investing with a longer-term horizon.

But the problem may be more fundamental, even structural.

We now have a pretty large economy which has grown between 6-7% for three decades. Despite some reforms, corporate lobbies have ensured that large parts of the economy are still protected. Import duties are higher than in most competing economies.

So with nominal growth at 11-14%, companies can continue to grow at high rates, maintain RoCE levels above 20%, and keep generating cash. So why invest?

This is an extremely short-term view. We should not think only of investing for India, but for the world.

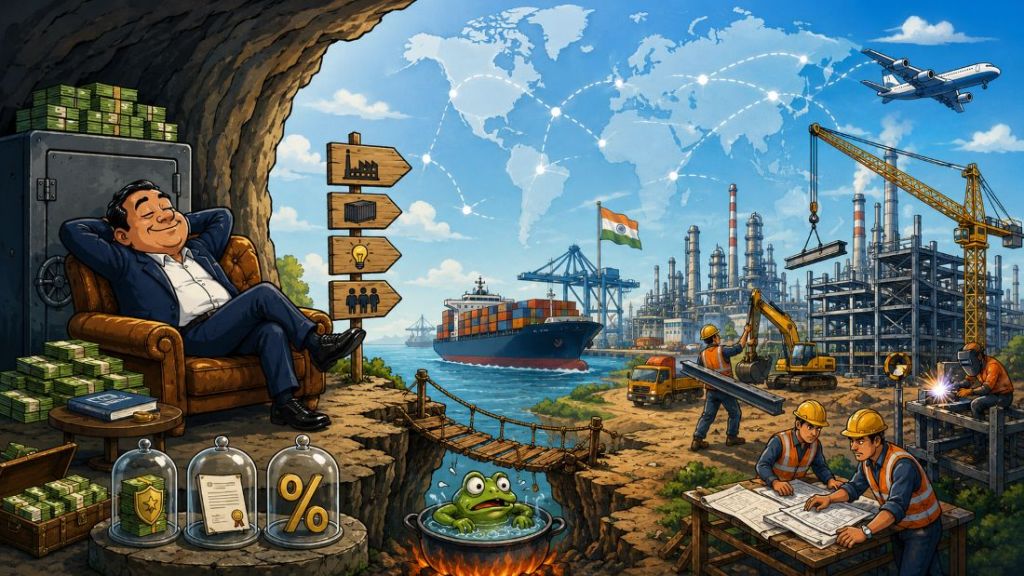

The argument that the market does not reward risk-takers is untrue. Some of the biggest wealth creators have been companies that invested aggressively for growth. Reliance’s Jamnagar refinery is a case in point. They built capacity far in excess of Indian demand. Their economies of scale (it is the largest single-location refinery in the world) allowed them to compete globally. Today, Reliance is India’s largest exporter, accounting for around 7% of merchandise exports.

Similarly, Adani built ports at a time when few dared to invest in such long-gestation, “risky” projects. Today, they account for 27% of India’s seaborne cargo and 45% of container traffic. JSW is another example in the steel industry. India’s pharmaceutical and auto industries have also shown that we can succeed internationally. Bajaj Auto gets around half its revenue from outside India. The common thread is that they all invested ahead of demand.

It’s not just about growth and profits. The danger is that we will never become competitive in manufacturing. In industry after industry, we risk obsolescence. We’ve been unable to take advantage of the China+1 tailwind, because we don’t have adequate capacity or capabilities.

Without investing, we will not develop the manufacturing ecosystem that we need. Recall that our globally competitive auto-comp sector was seeded by large Capex (Maruti and later, others). We need to do the same thing in every sector.

If not, we will become even more dependent on others for most of what we consume. In an increasingly fragile geopolitical climate, this will make us more vulnerable.

We have already seen this in solar, lithium batteries, semiconductors, rare earths, pharmaceutical building blocks and many other critical products.

Our Asian competitors (especially China) built factories before they had customers. Indian companies seem to want customers before building factories.

This may appear less risky. But the bigger risk is that orders may not come our way if we don’t invest in capacity or R&D.

By focusing on short-term RoCE and free cash flow, companies might be able to protect near-term share prices, but risk destroying long-term competitiveness. This will destroy “terminal” value – which is actually a larger determinant of valuation than medium-term earnings.

The metaphor that comes to mind is the “boiling frog” analogy. If Indian industry waits too long and the water boils, they may not be able to jump out.

Leave a comment