In the last few years, India has significantly ramped up Capex in the power sector, be it solar, grid connectivity, transmission and distribution infra, and more.

Total power generation capacity more than doubled from 248 GW in 2014 to 520 GW today. Within this, solar has jumped from 2.8 GW to 110 GW.

The transmission network has grown from 2.9 to 5.1 lakh ckm, while transformation capacity has moved from 5.3 lakh MVA to 14.2 lakh MVA. Millions of new homes have been electrified, and energy consumption has shot up.

Government intent continues. Power generation Capex is expected to more than double in the next five years to 2032. Ambitious targets have been set for renewables, nuclear, grid upgrades, smart metering, power storage, etc. EVs and data centres will further drive demand.

This is reflected in the stocks of power equipment and component providers – suppliers of power plants, boilers, transformers, turbines, winding wires, transmission towers, capacitors, overhead conductors, cables, and a variety of parts.

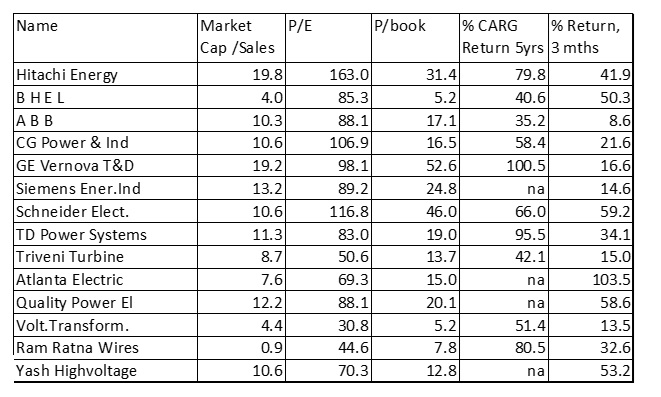

Data sourced from screener.in, 12 May 2026

Most of their stocks have provided amazing returns over the past few years (see table). And thanks to the current Gulf War, the push towards rapid electrification of the economy is now even more urgent.

The narrative is clear, and has legs to stand on.

But as an investor, the decision is not so clear (at least to me). Maybe I’m old-school and “can’t understand that this time it’s different”, but valuations of 100xP/E, 10xP/S, are worrying.

Such valuations usually reflect expectations of “perfect” execution.

What this means: Profits will grow at ~25% per year for several years. Margins will hold, or improve, thanks to operational leverage. Fresh orders will keep flowing in. There will be no project delays, no raw material price shocks, no bureaucratic or payment delays. And there will be no increase in competitive intensity.

To justify current valuations, these companies have to quadruple or quintuple profits in the next 5 years. It’s possible. But is it likely? And will all succeed?

Grey haired investors like me are always skeptical of absurdly high valuations. I don’t doubt that growth will happen. But it may not be linear – there will be unexpected speed-bumps that nobody can predict.

Also, such high growth always attracts fresh capacity – everyone wants a larger slice of the pie. This leads to higher debt or equity dilution. New capacity takes time to absorb, and initially depresses return ratios. Some projects will get delayed, and some customers will delay payments. Working capital needs will increase.

Again, I am not doubting the potential growth opportunity. It is real! India will see a boom in electrification over the next decade – from EVs to energy storage to induction cookers.

But will you make a lot of money buying stocks at 100+ PE ratios? Where is the margin of safety? Will valuations sustain if there is a bad quarter, or two?

Value investors may be better off looking in pockets where others are fearful, not where everybody is bullish.

I am not a registered research analyst or advisor. The above article should not be construed as investment advice or recommendation, but is merely for the purpose of debate and discussion. You should assume that I’m biased and may have a position in any of the stocks mentioned in the article.

Leave a comment