In recent weeks, much has been written about the great IPO frenzy of 2025, with analysts and fund managers warning retail investors not to take undue risk. The latest trigger has been the Lenskart IPO, which many wise men have termed as being excessively overvalued.

Yet, when I read most of the doomsayers and experts, they appear to be applying long-term investing lenses to a short-term profit sport. They assume that the investor wants to hang on to their shares for a decent amount of time.

The so-called retail investor is not really “investing” in IPOs, but speculating. Very few, if any, plan to hold the stocks. They’re looking to exit on listing day, hopefully at a profit. This behaviour is described as risky or careless. But does risk-taking automatically mean irrationality?

The reality is that listing gains over the past 5 years have been great. Most years have shown high double-digit average gains, and SME IPOs have done even better. Skeptics will argue that a few disproportionate gainers skew average gains and that allotment ratios vary widely, so average is not a good measure.

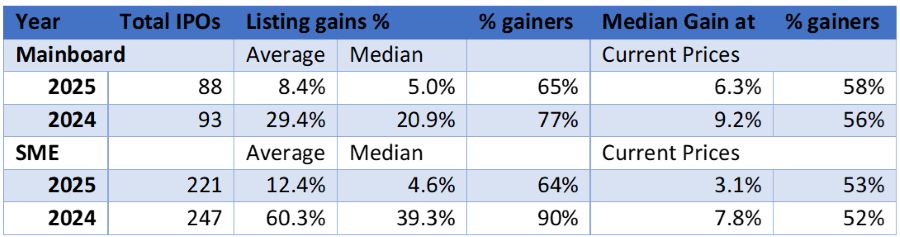

Data sourced from chittorgarh.com, 2025 data till end Oct.

Let’s look at median gains. In 2024, if an investor invested (and got allotment) in every mainboard IPO, half the investments would have gained more than 20.9% and 77% of the stocks listed at a premium.

For SME IPOs in 2024, the hit rate was even better. 90% of the stocks provided listing gains, and the median gain was 39.3%. Average gains were a whopping 60%.

And remember, these are not annual gains, but profits earned in a fortnight! If you can smartly roll over your money, annual gains could be substantial. Little wonder that people are borrowing to subscribe in IPOs.

There is, of course, the problem of over-subscription. If too many people jump in, your odds of allotment are very low. Further, higher-quality IPOs are often heavily oversubscribed, so your chances of allotment are lower. On the flip side, money remains in your bank account until allotment, so most retail investors are happy to keep small amounts in the savings account and play the lottery.

So where’s the downside?

Well, all good things can (and do) come to an end. Eventually, blind investing means that more IPOs will come in at ever higher valuations, and a flood of IPOs will suck out liquidity. Some of this is already visible in the lower returns we see in 2025 (to date).

Remember that for the hypothesis to continue working, we don’t just need investors in IPOs; we also need people who are ready to buy immediately after listing. If this doesn’t happen, listing (and subsequent) gains will fall.

Interestingly, if you look at the 2024 and 2025 IPOs at current prices, the gains are not so good (assuming you had held onto the shares). Look at the 2024 data, where stocks have been listed for around a year. Median returns fall to single digits, and just over half the issues quote higher than the issue price.

Data sourced from chittorgarh.com, 2025 data till end Oct.

The data suggests that (roughly) a year later, many stocks are unable to hold on to listing day gains. This clearly tells the investor: “Hey, no point in holding. Simply exit on day 1”.

Some people (like me) believe in investing for longer durations, and usually avoid overpriced IPOs, but this does not mean that all IPO investors speculators are being irrational. The party will end sometime, but as long as it lasts, who’s to question why?

Maybe the real irrationality lies in expecting speculators to behave like investors.

Maybe IPO investors aren’t losing their minds — but just playing a different game.

Leave a comment