I recently read an article claiming that fintechs and NBFCs will use AI to dominate lending, while traditional banks fade into irrelevance.

It sounded plausible at first. But the more I thought about it, the less convinced I became.

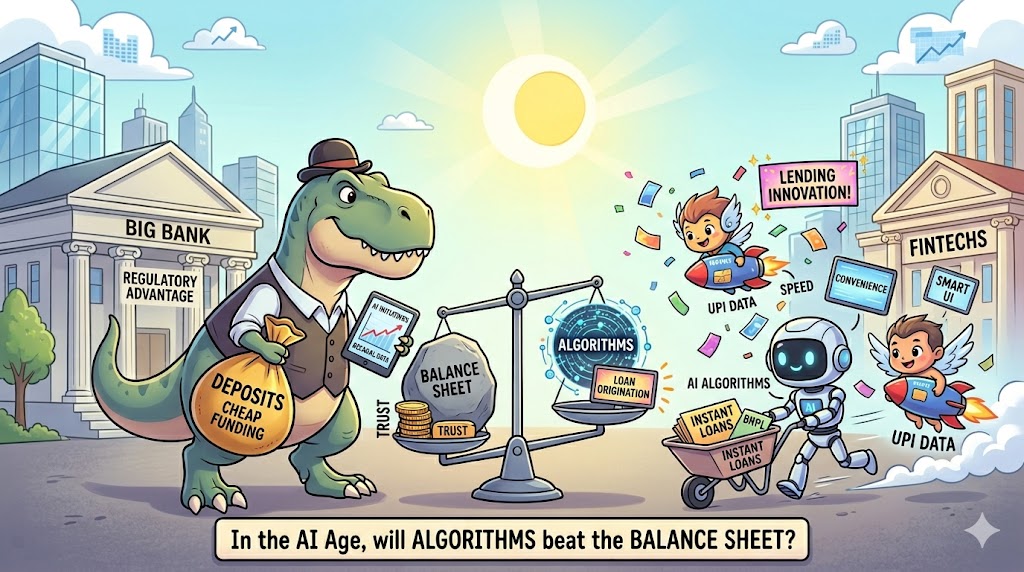

The essence of the argument is as follows: Today’s consumer wants speed and convenience (i.e. instant loans) and values the UI more than the branch. The rapid growth in BNPL and other small-ticket loans is cited as evidence.

Growth will continue to be driven by tech-first, young consumers and underserved segments (such as the self-employed, SMEs, and microfinance) and smaller towns. This is where the fintechs’ ability to use AI and UPI data to provide quick, apparently low-risk loans will be a huge advantage.

And so on.

All this got me thinking. Are banks not using AI? Can’t they also do this? Is the branch network really a liability in tomorrow’s world? Will banks really become irrelevant?

Lots of questions – let’s go one by one.

Large banks like HDFC, Kotak, ICICI already run multiple AI initiatives – often at significant scale. More importantly, they have the balance sheet to keep investing.

AI agents are being used to streamline legacy processes, saving cost and time. Banks have vast “data lakes” from decades of customer history. They can mine this data to predict what you might buy next. AI is also being used to speed up the diligence process and improve customer communication.

The fintech camp believes that nimble start-ups are way ahead in tech/AI, while large, sleepy(?) legacy banks are not so innovative. I won’t comment on that, except to point to the issue of diminishing returns.

The popular view is that early and smart AI adoption will lead to ongoing gains as the AI improves with more data. However, it’s also possible that once the low-hanging fruit has been harvested, each additional Rupee invested may yield lower RoI. If so, some banks may well catch up.

This is typical in any new technology wave, though experts say that “AI is different!”

But beyond technology, the biggest advantage that banks have is cheap funding. You might borrow from a fintech, but will you keep your money and deposits with them? This is a trust issue, and physical branches still provide comfort to depositors.

Another issue is loan quality. While algorithmic lending sounds great, not everybody’s algorithm will be equally good at avoiding default – especially across economic cycles. The mad race for market share might dilute standards, as happened with some banks.

This will become clear over time, though early warning signs suggest possible distress down the line for BNPL or small-ticket online loans.

Our regulator (the RBI) is naturally risk-averse, and wants loans to be underwritten by banks – which effectively limits many fintechs to loan origination or cross-selling.

Disruption is evident. Many smaller, sleepier or tech-challenged banks may not be able to compete. But this does not apply to the entire sector.

I am not suggesting banks are brilliant investments. Competitive forces have increased dramatically in the past decade. The banks’ share of profit pools is falling, and alternative investment avenues (mutual funds) are hitting deposits.

NBFCs too are larger and better funded – Bajaj Finance and Jio Financial are bigger than many banks. Corporate borrowers, too, have more options, including bonds and private credit from PEs.

The most likely outcome is that a few of the incumbent banks and large NBFCs will better exploit these disruptive technologies, leveraging their strong balance sheet, customer base and regulatory advantages. Some fintechs will also scale and compete; a few will acquire banks or bank licenses – but not all of them will make the transition.

Time will tell, but I wouldn’t write off banks too soon.

Leave a comment