The current Middle East crisis is not merely about oil and fuel, but a massive inflation shock rippling through the global economy.

Reduced supply has triggered price spikes in petrol, diesel, aviation fuel, gas, fertilisers, and downstream chemicals. It’s not just oil derivatives—critical industrial inputs like aluminium, helium, methanol, sulphur and ammonia are hit as well.

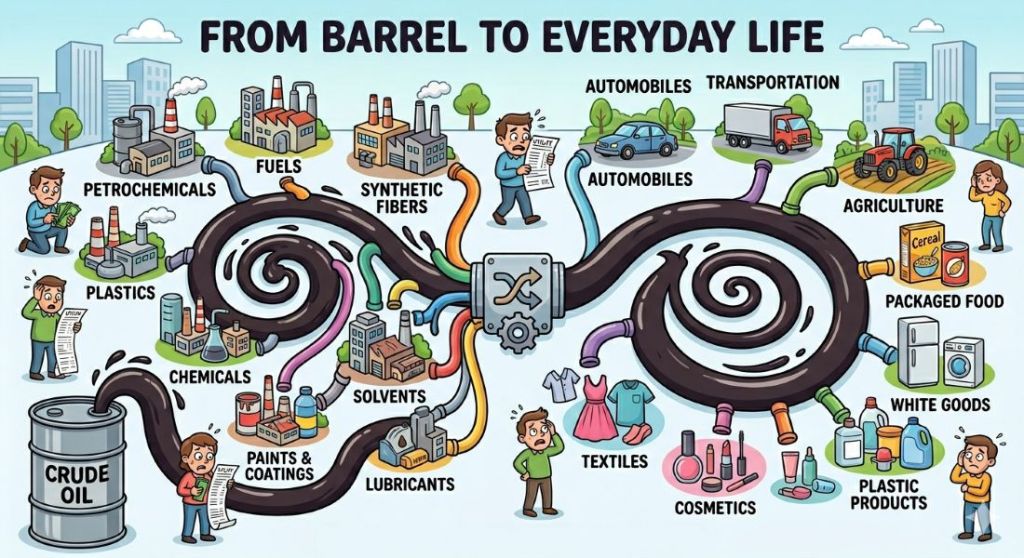

The obvious shocks are clearly visible.

Rising fuel costs and insurance have inflated shipping costs, impacting almost every commodity and traded product. Many countries have raised petrol and diesel prices.

Restaurants in India are shutting down due to LPG shortages. Tourism across Asia is hurting due to the disruption at Middle East airline hubs, and airfares are rising. Tile makers in Morbi have shut down. The story echoes in every corner of the world.

But fuel is only the tip of the iceberg.

The pain is being further distributed by downstream chemicals that sit at the heart of modern manufacturing.

- In automobiles; plastics, paints, synthetic rubber, carbon black, solvents and lubricants are all part of the petrochemicals chain. Car prices must go up, or margins will fall.

- Refrigerators use PU, polymers, coatings, and refrigerants – all now costlier. The same applies to washing machines, ACs and other products.

- Paints, pesticides, and dyes are similarly affected – pushing up costs for construction, agriculture and textiles (which are already hit by polyester price increases).

- Packaged food, cosmetics, and most FMCG products rely on plastics, surfactants, solvents and base oils.

- All transport will cost more – not just airlines, but buses, cars, taxis, 2-wheelers and rickshaws.

- Higher cost of APIs, solvents (like methanol and acetone), and packaging will squeeze margins for pharma companies.

- Even engineering depends on greases, oils, coatings, finishing chemicals and electrodes – apart from metals. Steel needs coking coal. Everybody needs energy.

The reach is near-universal; no supply chain remains untouched.

The real issue here is the second-order impact. Rising input costs will percolate across sectors, including agriculture. Eventually, the customer will have to pay.

Demand could weaken if customers are reluctant to buy at higher prices. If our government continues subsidising fertilisers and fuel, deficits could widen, or spending elsewhere could shrink. Rising inflation will also limit central banks’ ability to cut rates, even as growth slows.

This is not a happy situation, to say the least!

There are, of course, silver linings. Some Indian chemical companies with multi-fuel capabilities and captive/domestic raw materials are now more competitive against imports. Expect the market to reward companies with bargaining power and the ability to maintain margins through superior supply chain integration or energy-frugal operations.

Some sectors may actually benefit from increased demand – notably energy producers, capital goods suppliers to alternate energy and electrification, and of course, defence. [Caution: Valuations may already reflect some of this.]

But the negative impact on the economy is much greater. And there’s not much that you, or I, or even the government can do. For businesses and investors, we need to manage the situation as best possible, and build longer-term resilience.

Unless of course, you can convince Mr. Trump to end this war!

First published on indianotes.com

Leave a comment